How (and why) art museums, auction houses, and galleries collaborate

This is how the art business works...

Hey there,

I hope your summer is off to a great start. I’ve spent the last month in finals and decompressing after a productive semester, only visiting a few exhibitions. Thus, I’d like to focus on the Art market, briefly explaining the industry’s high prices and opaque business models. In addition to this, I’ve included a great exhibition at the bottom of the email.

One of my first experiences with the volatile New York art market was in Fall 2017, which was an exciting time for art dealers. At the end of the year, those with major assets in art were buying, each looking for works worth six, seven, or even eight figures. In the final weeks of the year I saw financial professionals and lawyers among major collectors abound with art assets looking to move money around. What brought them there? It wasn’t a rockstar artist’s blockbuster exhibition nor holiday shopping. It was the Trump administration’s Tax Cuts and Jobs Act, taking effect January 1st, 2018. A tax loophole was driving art sales at this unique time, and I’ll explain why at the end of this post.

As a scarce luxury good, it makes sense that art can be stored, traded, or sold, while rising and falling in value. The art market, like any market, is a fast-paced system vulnerable to volatility. Knowledge of these mechanisms can improve reform and critique of the art economy, or help prospective art buyers make educated decisions aligned with their values and interests.

Important to understanding the art market are three “laws.” First, institutional validation legitimizes cultural and historical relevance, and, thus, price. Second, auction houses sell publicly to whoever will pay the most, and galleries privately “place” (sell) artwork in (to) collections. Third, all artwork is either primary, meaning directly from an artist or estate, or secondary, meaning that it was previously bought and sold. While auction houses and galleries can sell primary or secondary, auctions focus on secondary markets, and gallerists and dealers focus on primary markets.

Galleries build and protect an artist’s market, facilitating the pipeline from studio, to private collections, to museums. This means selling art to collections unlikely to resell, diminishing the supply, and hopefully leading to museum donations at a later date. Galleries set prices and auctions can affirm or challenge these valuations in a public setting.

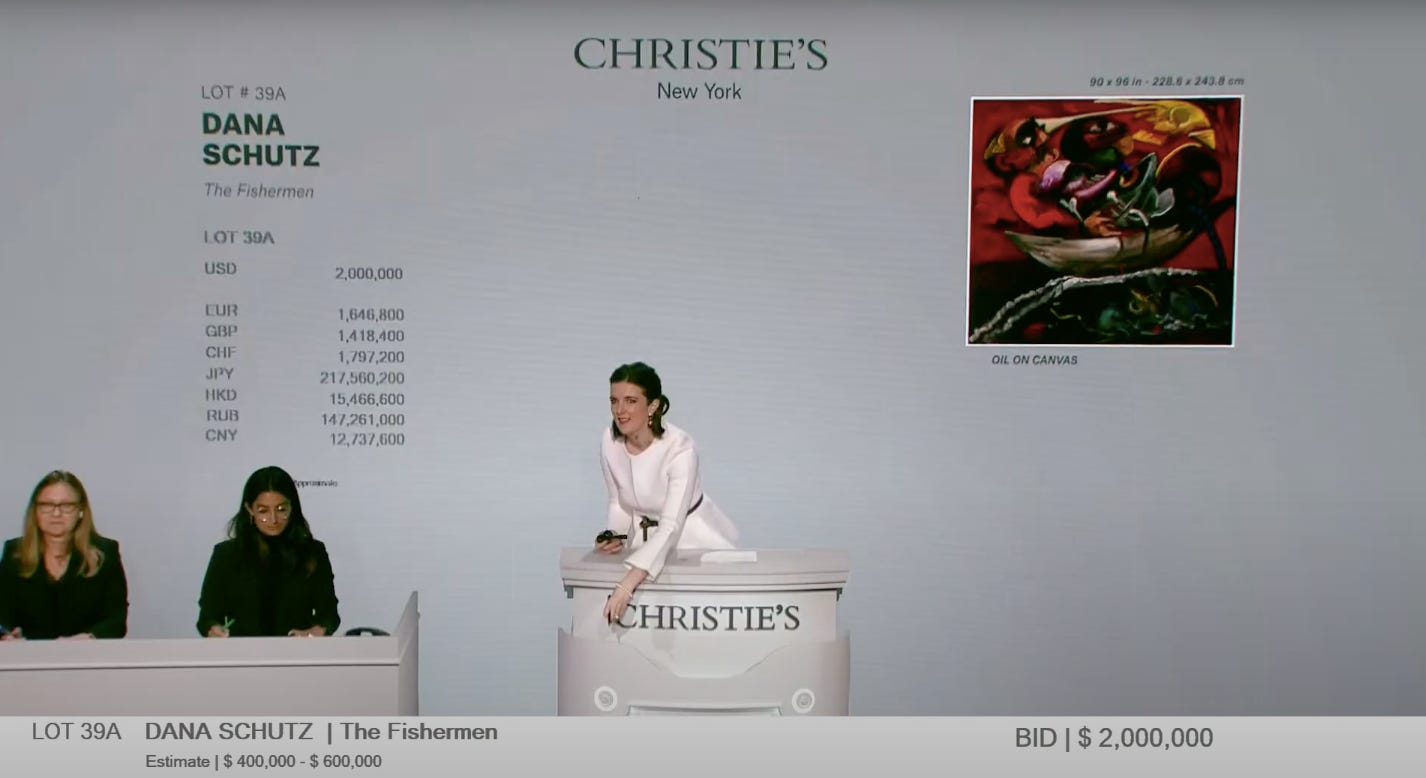

As I mentioned in last month’s newsletter, David Zwirner showed new work by Dana Schutz at Frieze, pricing each of the five paintings around $750k. In a very smart strategic move, they put a work up for auction at the end of the week, donating the proceeds to a not-for-profit aligned with the values of the artist. While this is a charitable move, all parties benefit. The painting sold at auction for $2.97 million, a fantastic opportunity to increase the future prices of Schutz’s primary work by, likely, around 50%. This allows the gallery to build her market while maintaining control of who they sell artwork to. It’s the ultimate win-win-win.

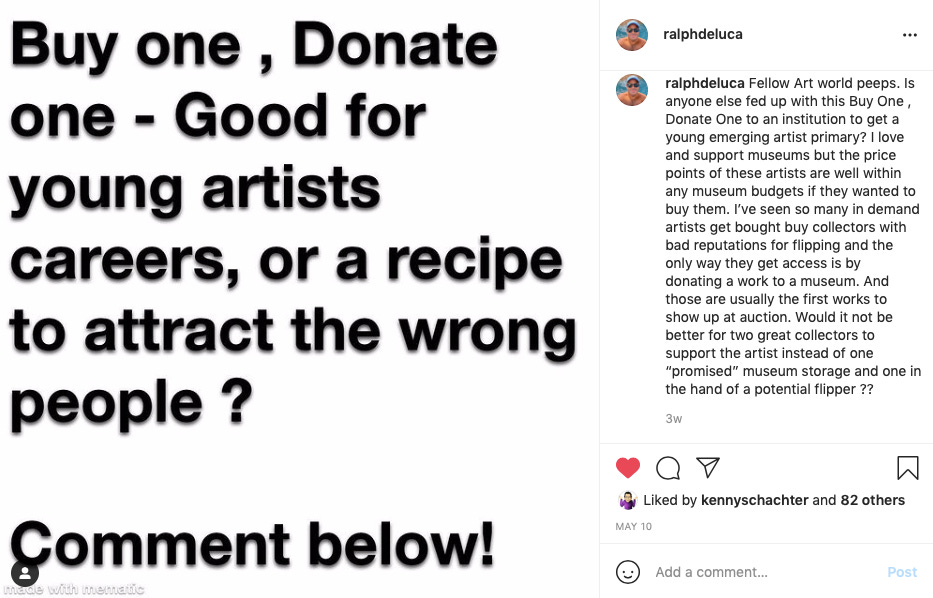

Now, galleries may require a client to donate a work by a popular artist to a museum before they’re able to purchase the artist’s work for their own collections. Unfortunately, this can lead to works getting in the hands of collectors only interested to flip the work at auction for profit. For this reason, many galleries have clients sign no-resale contracts, limiting a buyer from reselling an artwork in a specified time period. When an artwork is frequently bought and sold, collectors might infer it is low quality. Despite the un-enforceability of these clauses, the reputational cost is clear.

What does this structure of transaction mean for our art and cultural institutions? Galleries are attempting to decrease the friction for a museum to acquire an artwork. At the same time, transactions are changing our institutional infrastructure. Do major galleries staging “museum-quality exhibitions” confer institutional significance? What about art collecting families who start their own private museums? The public and private in art continues to blur, but it always has.

The MoMA started as a group of private donors, while the Whitney Museum was founded on the patronage of collector Gertrude Vanderbilt Whitney.

Galleries often advance the production costs of an artist’s studio, with the intention of recouping this investment when they sell work. An artist’s gallery prefers to maintain control over the collections which can acquire an artwork, offering a discount to the right collection or choosing to sell the work for less than they’re able to. An artist in a strong collection, or group exhibition at an important gallery or museum, can indicate who has eyes on their work and even hint at the trajectory of their career.

Josh Baer, who writes a private art market newsletter, sometimes publishes the buyers of otherwise private sales or the names of underbidders on major works at auction. This information is invaluable to art dealers: if you know Alex is looking for an early Warhol, you can leverage your network to offer them a strong work another dealer might not have access to, unaware of a motivated seller and the interested buyer. With a similar intention, dealers keep an eye on Architectural Digest: an art buyer’s tastes and available wall space might be surprisingly accessible information.

While the strategy of artists, galleries, and estates is important to the visibility of an artist, the saving grace of this complicated narrative is that the greatest art floats to the top. In my own art buying I purchase what resonates with me personally, on various levels, sometimes selectively factoring qualitative metrics such as museum representation. There is a clear methodology to buying art which can be sculpted in concert with an art buyer’s goals and values.

It is important to contextualize and understand the art market pipeline to make educated decisions, especially when prices can materially influence lifestyle and financial security. Historical and cultural narratives go in and out of style, as does the influence of museums. Time shows unwavering influence in the art business, and the arc of art history bends towards the public.

The reason people were buying art at the end of 2017 was because the Tax Cuts and Jobs Act changed the legal parameters for “like-kind exchanges.” This law allows someone to defer paying tax on the appreciation of an asset, if that asset is exchanged for the same kind of asset (in this context, another artwork). For example, let’s say Alex purchases a painting in 2013 for $50,000. In 2016, they are offered $70,000 for the work. Alex could use the proceeds of this sale towards another painting, deferring the payment of capital gains tax on $20,000 of appreciation. There are many nuances to this kind of transaction, but this is the basic mechanism.

While like-kind exchanges are still a part of the tax code, you can no longer perform them on art or personal assets. The final months of 2017 were the last opportunity for collectors to take advantage of this law, driving many into galleries to shop for the next great work of art, lowering the risk of their acquisitions, incentivizing the acquisition of new assets. Galleries were able to re-access great supply and collect an additional commission on an artwork they’ve sold before.

Let me know what you think and how you’re doing. Stay well.

Yours,

Gabe

Exhibition

Seeing Eamon Ore-Giron’s most recent solo exhibition last month was most rejuvenating. They’re intricate, attractive paintings of daunting scales, meditating on pan-American aesthetics and two major personal events in the artist’s life: the death of his mother and birth of his son. These events are the reason for the name of the show, The Symmetry of Tears. Ore-Giron is engaging aesthetics in Andean historical and cultural canons, reformulating this vocabulary of abstraction in a new context. He uses gold (the color) as a material demanding re-contextualization, challenging the relationship between aesthetics and history.

Courtesy: James Cohan Gallery